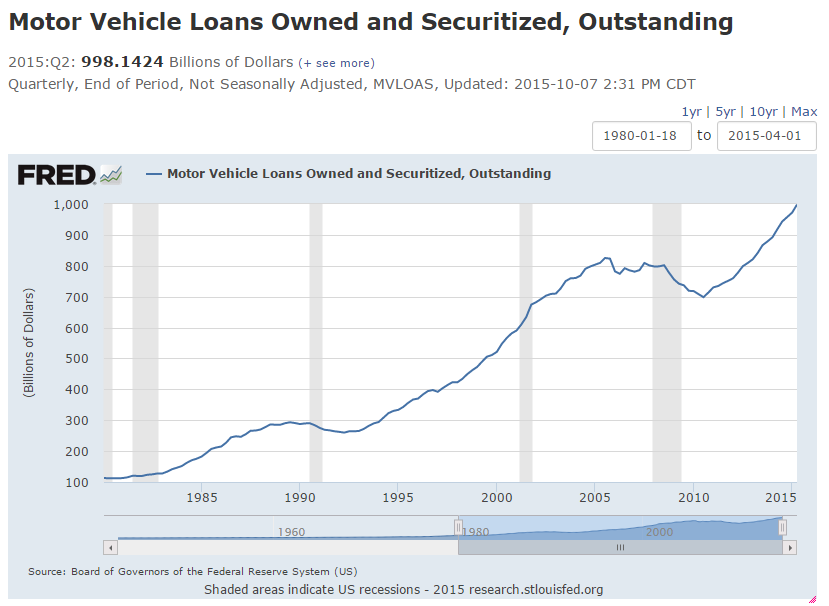

I’ve seen some recent reports on the record amount of auto debt in the U.S. financial system floating around the web. Most of the reports reference, in one form or another, the following chart showing motor Vehicle Loans held by U.S. financial institutions.

While this measure arguably misses some of the vehicle loans in the “non-traditional” lending channel (shadow banking anyone?), it’s still a good representation of the growth in auto debt in recent years. Since the last peak (which was 12/31/05), auto loans have grown just over 21%.

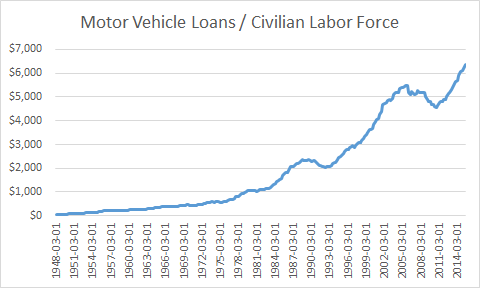

However, what we also need to mention is that population has grown as well. Below I show the amount of motor vehicle loans divided by the civilian labor force. I used labor force under the assumption that only people with a job can qualify for a car loan (a dubious assumption I know, but just go with me here).

What this chart tells me is that the average working person in America has $6,356 worth of auto debt. This compares to about $100 of auto debt per American worker back in 1950.

Since the last peak (12/31/05), auto debt per worker is up just shy of 16%. While still a sizeable jump, it's better than the 21% headline growth since 2005.

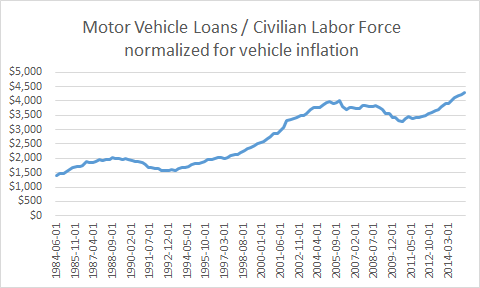

Of course, thinking about the growth in debt per American worker since 1950 got me to thinking about how much a car cost in 1950. The internet (they have that on computers now) tells me that a new car cost $1,510 in 1950. Today, the average new car costs $33,560. A 22 fold increase in car prices has been met with a 64 fold increase in vehicle debt per worker.

So I downloaded consumer price index (CPI) data on new vehicles. Unfortunately, the data only goes back to 1984. Nonetheless, if we normalize the auto debt per worker for the CPI on New Vehicles (debt/workers/(Auto CPI - 100)) we get the following chart:

Normalized for inflation, the average U.S. employee had $4,010 of auto debt in December 2005 (previous peak) vs. $4,309 today, for an increase of 7.4%. While still growth, a 7% increase in the last decade is a far cry from the 21% growth in the headline number above.

I’m not sure what the takeaway is here - I need to think more about these numbers and what they actually mean. Probably the best takeaway, as usual, is that this business of investing is simple, but not easy.

Please feel free to respond and/or correct any gaps in my thinking.

Harvest Investor © 2015. All rights reserved. The content and ideas contained in this blog represents only the opinions of the author. The content in no way constitutes investment advice, and should never be relied on in making an investment decision, ever. No content shall be construed as a recommendation to buy or sell any security or financial instrument, or to participate in any particular trading or investment strategy. The author may hold positions in the securities and companies mentioned on this site. Any position disclosed on this site may be modified or reversed without notice to you. The content herein is intended solely for the entertainment of the reader, and the author.

5 comments:

What has me scratching my head is that the average age of the vehicle is also increasing at the same time as debt.

http://www.rita.dot.gov/bts/sites/rita.dot.gov.bts/files/publications/national_transportation_statistics/html/table_01_26.html_mfd

I just bought a new car, and several models had 0% financing without any cash incentive. So you could pay x over 5 years or x today. Sort of seems like the car companies are pushing their profits into their finance arm.

Chris: Very good point. It seems that banks are extending out loan maturities in recent years to entice more loans.

Like you, I've been frustrated by the lack of ability to get a discount for paying in cash - there is a disconnect in the system between the dealer and the financial arms.

Do the car companies have a tax incentive to move profits to finance? I view their finance arms as a great source of risk for the car OEMs.

I made a mistake in that sentence, by charging 0% they are pulling profits out of the finance arm. Either way, I'm not aware of the tax effects.

I agree with the increased risk, especially when the finance arm is being used as a sales tool!

I know of no tax incentive for the finance arms (although I should research this further), with the reason for using them being both a sales technique and a driver of profits (banking can be very profitable when done right). John Deere's (DE) financing arm has been very successful (and very safe in the past). However, like any banking/financial institution if the incentives get misaligned (if sales take precedent over credit culture), very bad things can happen.

Post a Comment