Conversions have a long and storied history on Wall Street. Seth Klarman in his famous book, Margin of Safety, outlined their attractive economics ("as long as the preconversion thrift has a positive value"). Peter Lynch did likewise in Beating the Street. Yet since you're often dealing with small- and micro-cap names, they remain a cult investment.

I have historically dabbled in this market with some successes and a few not so successes. Finding a good, repeatable, strategy when it comes to Thrifts has, however, alluded me. Strategies that I have seen recommended by other investors include:

- Buy the whole complex (i.e. buy every new Thrift IPO).

- Lingering questions: how long do I hold these positions? What causes me to sell? How to I manage portfolio allocations?

- Focus on the takeover candidates.

- Lingering questions: Do I wait until the IPOs are seasoned for three years (regulatory rules usually prohibit acquisitions for 3 years)? How long do we wait for an acquisition? What key criteria are acquirers looking for?

- Follow the activists (Stilwell, Seidman, etc.).

- Lingering questions: What are their criteria for ownership? Is coat tailing sustainable, or will I panic at an inopportune time since it's not "my" idea?

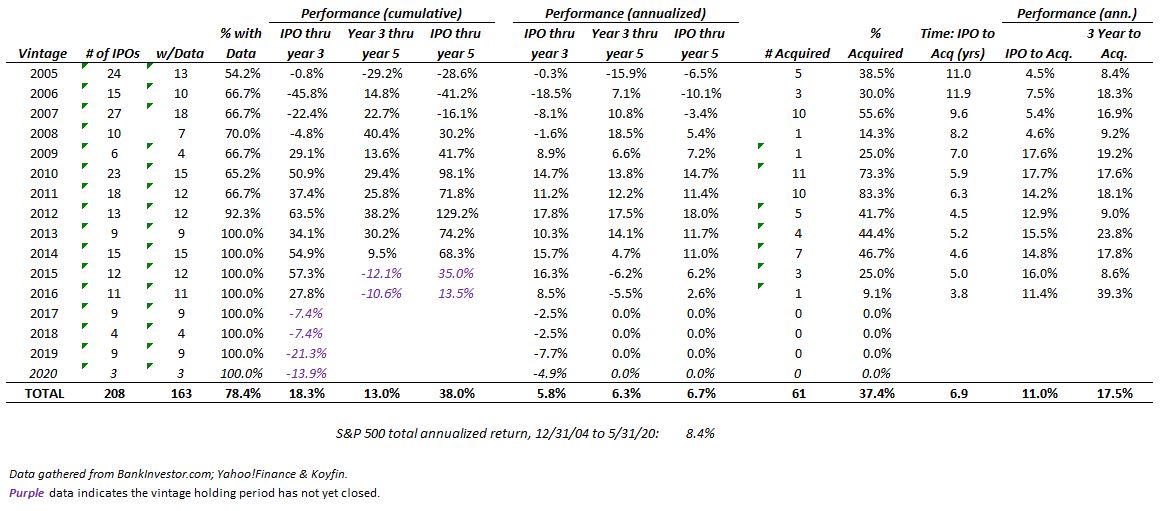

For that reason, I went back and looked at every single mutual bank IPO (as listed on bankinvestor.com) from 2005 to today. I then looked at those banks performance in the first three years after IPO, years 3-5, and an overall performance (IPO to 5yr). I also looked at how many were acquired, how long it took for them to be acquired, and their performance.

A few caveats: this is an "in bulk" analysis - glossing over the vast differences between all of these banks. It also ignores the differences between 1st step conversions (to a Mutual Holding Company structure) and 2nd step conversions (from MHC to stock company). Also, there is some survivorship bias. I wasn't able to get price data on every single bank (the farther bank you go, the worse my data capture became).

For ease of comparison, I grouped them by year - creating Thrift IPO vintages. See the following table.

A few takeaways:

Harvest Investor © 2020. All rights reserved. The content and ideas contained in this blog represents only the opinions of the author. The content in no way constitutes investment advice, and should never be relied on in making an investment decision, ever. No content shall be construed as a recommendation to buy or sell any security or financial instrument, or to participate in any particular trading or investment strategy. The author may hold positions in the securities and companies mentioned on this site. Any position disclosed on this site may be modified or reversed without notice to you. The content herein is intended solely for the entertainment of the reader, and the author.

A few takeaways:

- From 2005 to the end of May 2020, the S&P 500 total return was 8.4% per year. Thrift IPOs (assuming you held for 5 years and kept rolling your portfolio into new names) returned 6.7% per year [in fairness, this is a price only return - dividends may have added to the performance]. Right off the bat, we're behind just buying an index fund.

- Thrifts, like most all of the market, are subject to cycles. Buying vintages 2005-2009 (IPO'd into or during the Financial Crisis) did very poorly. Vintages 2010-2014 did very well.

- Whether by cause or effect, the 2010-2014 vintages had very high acquisition rates. In a strong economy acquirers were looking for solid deposit bases and growth opportunities.

- In recent years (vintages 2014-2016), you would have done better buying new IPOs and holding for three years. Historically, however, that trend reverses, and you would have done (marginally) better buying seasoned banks three years after IPO (opening the acquisition window).

- There is some (limited) evidence that buying seasoned banks after a drawdown may have merit. The 2007 & 2008 vintages recovered nicely from the Financial Crisis in years 3-5 of their lives.

- 37% of all thrift IPOs are eventually acquired, but the average time from IPO to acquisition was 6.9 years (or 3.9 years from when the acquisition window opened).

- If you can identify the acquisition targets (a very big IF), their average return from year 3 to acquisition was 17.5% annually for an average of 3.9 years.

- Understand the banking cycle. There is a delay between when the banking cycle turns up, and outperformance in Thrift IPOs (due to them being acquisition targets). This is evidenced in the vintage 2010-2013 IPOs. They saw their best performance in the calendar years 2013-2016 as acquirers sought them out. Put another way, momentum for the whole community bank complex matters.

- Valuation and fundamental analysis are important. Buying the whole complex may work in certain instances, but it needs to be paired with attractive valuations and strong fundamentals. You need to understand the bank, its geographic region, and management incentives.

- Perhaps the biggest takeaway is that each of the strategies listed above: buy them all, focus on takeover candidates, follow the activists, etc., may each work at different points in the cycle. Be adaptable and disciplined enough to adjust for economic circumstances. Be willing to walk away from the sector when the stars don't align (and conversely, be willing to build positions when they do).

- I think there is value in going back and studying each of the banks that have been bought out over the last 15 years - I will add that to my research list.

Harvest Investor © 2020. All rights reserved. The content and ideas contained in this blog represents only the opinions of the author. The content in no way constitutes investment advice, and should never be relied on in making an investment decision, ever. No content shall be construed as a recommendation to buy or sell any security or financial instrument, or to participate in any particular trading or investment strategy. The author may hold positions in the securities and companies mentioned on this site. Any position disclosed on this site may be modified or reversed without notice to you. The content herein is intended solely for the entertainment of the reader, and the author.

3 comments:

Thanks this was very helpful. I would suspect that the returns would be better if the MHCs were pulled out.

Also, would be interesting to see an analysis done if you sold on IPO day, assuming you were a depositor and could buy at the IPO price.

Have you noticed the trading in bank conversions since 1/1/2019?

Conversions all priced at $10.00 per share and closing prices today:

2019 Bank Conversions:

BCOW $9.10

ERKH $9.76

FSEA $6.15, I bet those with a big allocation are real happy

HONE, $8.54, and they are in the same market as Eastern

PBFS, $9.15

PVBC, $7.86

RBKB, $6.56, those auto loans may not be the greatest idea in the world, will it trade over $7.00

RMBI, $11.24, well, at least this one in over its issue price!!!

TBBA, $6.61

2020 winners:

BSBK, $8.74, well, maybe it's not over $10.00

CNNB, $8.98, but it was over $10.00 for one day recently but it didn't stay there

FFBW, $8.60

Aren't these things supposed to trade over $10.00 a share to make us money?

Is there a typical acquisition structure, cash or stock in the parent company? If cash, was this included in the returns of the acquired companies? Thanks for the stats!

-Dan

Post a Comment